Intrinsic Value Assessment Of Whirlpool Corporation (WHR)

By Robert Leonard From The Investor’s Podcast Network | 16 March 2021

INTRODUCTION

Whirlpool Corporation (“Whirlpool”) (Ticker: WHR) manufactures, markets, and sells major home appliances across four segments — Asia, Latin America, North America, and Europe/Middle East/Africa. Its product portfolio includes refrigerators, freezers, cooking appliances, laundry appliances, and more, but its business is heavily dominated by laundry appliances, refrigerators, and freezers. While Whirlpool does sell many products under its flagship “Whirlpool” brand. It also has other popular brands in its portfolio, such as KitchenAid, Maytag, Consul, and Brastemp.

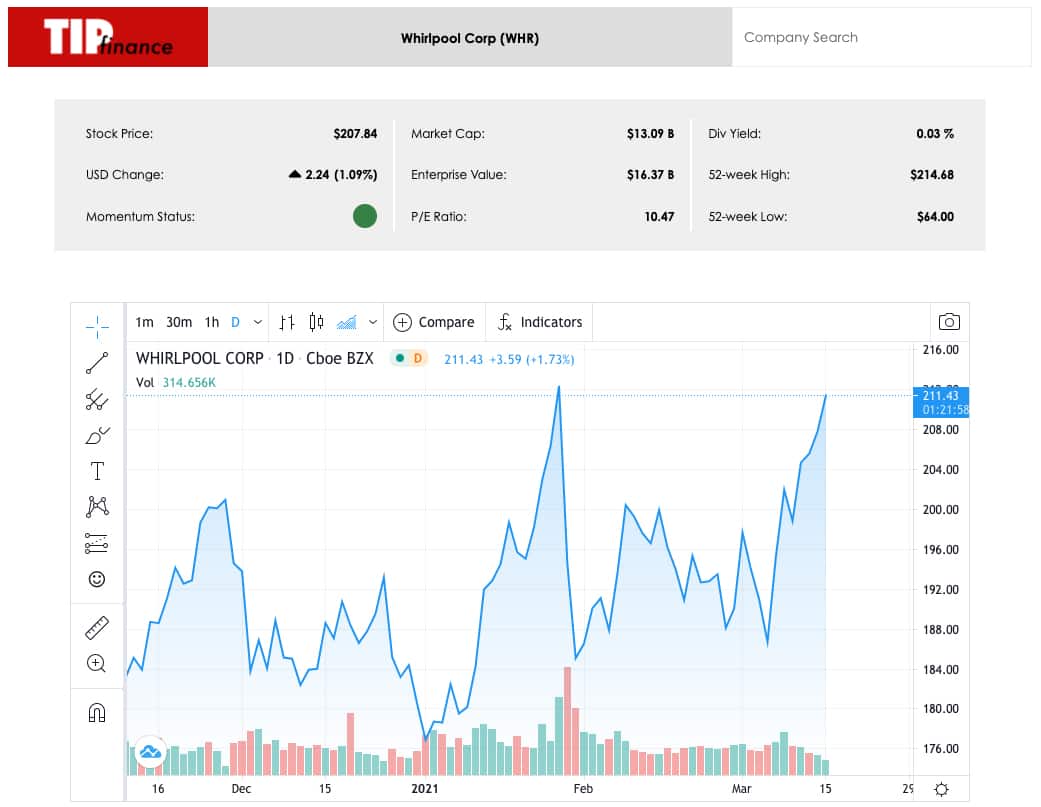

At the time of writing, Whirlpool’s market capitalization is about $13.27 billion and its revenue and cash flows for the 2020 fiscal year were $19.5 billion and $1.1 billion, respectively. Currently trading at $211.43, the stock has hit a 52-week low of $64.00 and a 52-week high of $214.68.

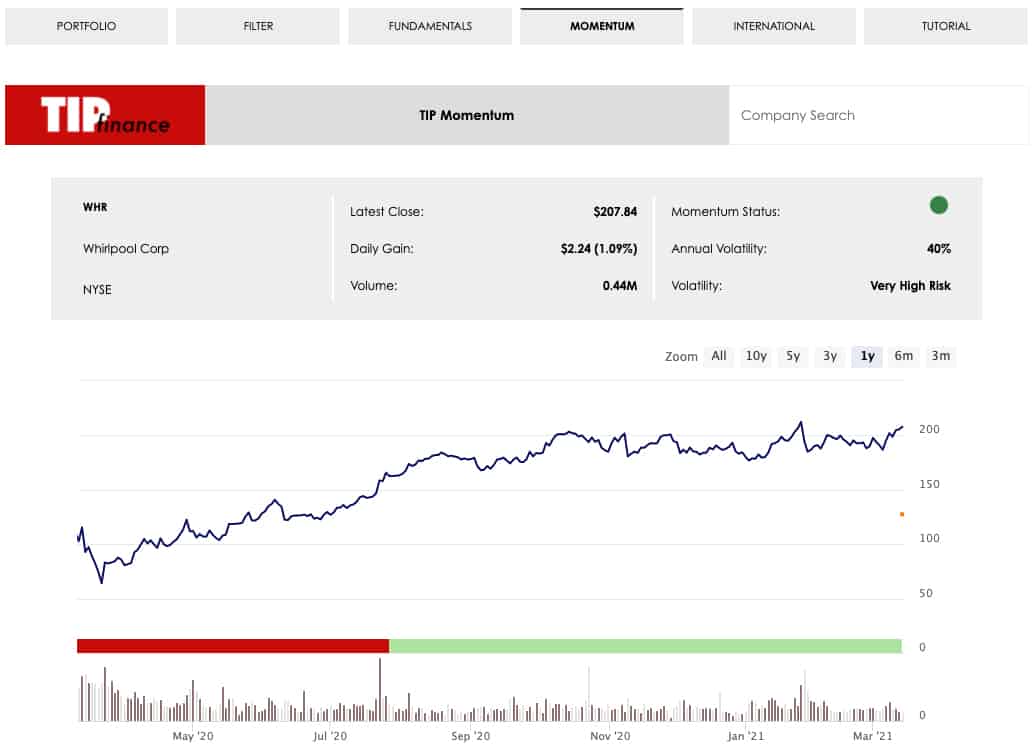

In our last Intrinsic Value Assessment, we looked at Autozone and I talked about how I was familiar with the business from the perspective of a customer but had never thought of it as a potential investment. It’s a similar situation with Whirlpool. As a homeowner and real estate investor, I’ve bought many appliances in my time, some of which were Whirlpool, some that were not, all giving me different perspectives on the appliance industry, companies, brands, and the appliances themselves. Then, the other day, I was using the TIP Filter function in TIP Finance tool as I researched for potential investment ideas when I came across Whirlpool trading at an attractive TIP Multiple, TIP Median Multiple, and a satisfactory Potential Yield, all with a green Momentum Status. I also thought about a recent newsletter I wrote about Peter Lynch and the advantage individual investors have over Wall Street.

Now the question is, at today’s price of $211.43, is Whirlpool’s stock undervalued?

INTRINSIC VALUE OF WHIRLPOOL CORPORATION

When we committed to writing a new Intrinsic Value Assessment every two weeks for the TIP website, I first wrote about a company that was about as far away from a traditional “value pick” as you can get, then the second one was far more in line with a traditional value investing stock pick. Similar to the most recent Intrinsic Value Assessment, this research report falls more in line with the traditional value investing thinking.

Why do some of these companies fit the mold of “value investing” better than others? Square is a high-growth technology company looking to disrupt an industry by continuing to innovate, whereas AutoZone and Whirlpool are much older companies, with far more stable and consistent results. Each of these investments can work, but they’re very different strategies and approaches.

In the analysis about Square, I wrote, “DCF models are often associated with value investing because they can be great to value a more mature company, which, historically, has been the focus of value investors. However, in the case of a company like Square, which is still growing rapidly and far from maturity, DCF models are far less useful. As investors, we must be a bit more creative in our valuations to accurately model these types of companies.

In the case of Square, it is a relatively early-stage company, making it difficult to use historical data, as well as traditional profitability numbers, to forecast its future results.”

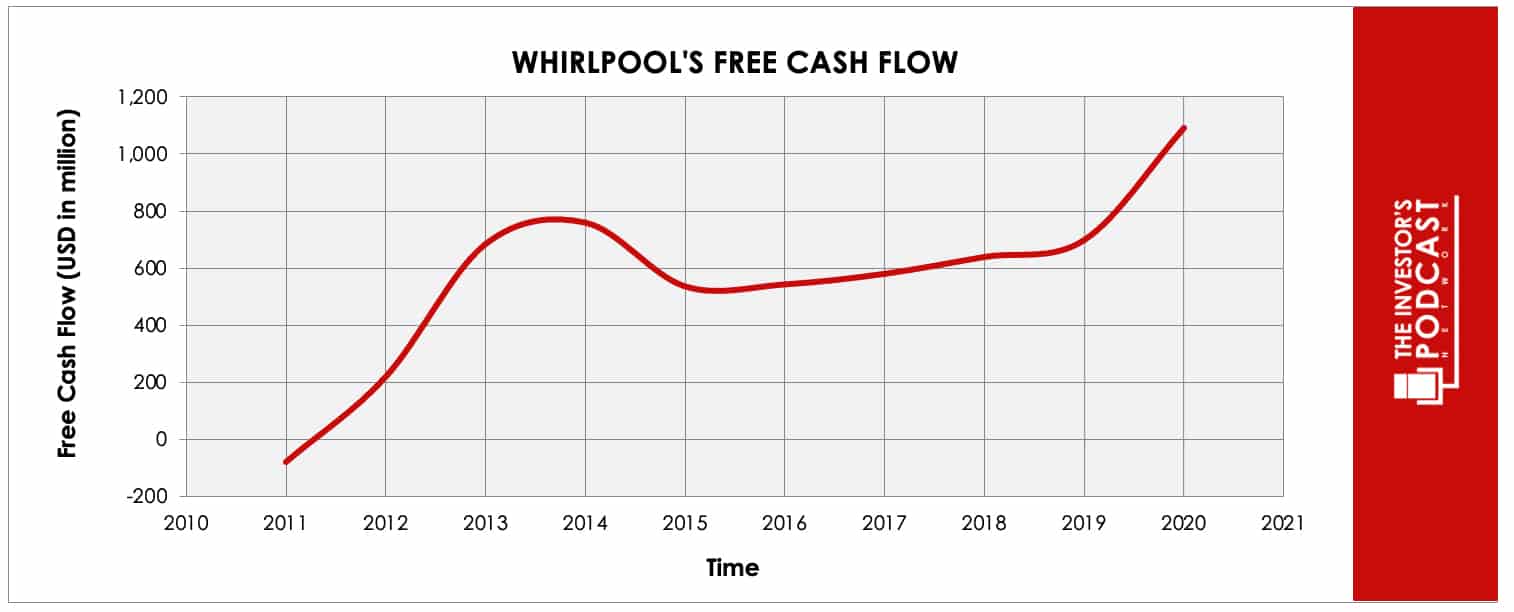

On the other hand, Whirlpool fits perfectly into the “box” for using a DCF model. In the below image, we can see how relatively stable Whirlpool’s positive Free Cash Flow generation has been.

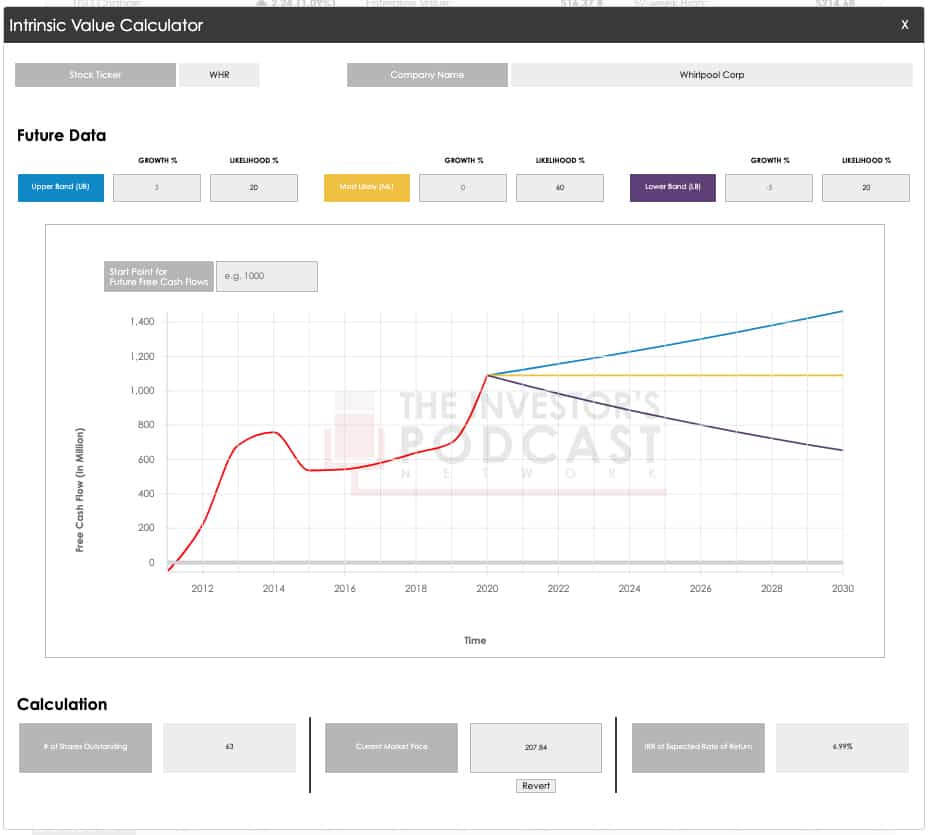

Let’s look at a potential DCF model for Whirlpool below.

This DCF model was run in our TIP Finance tool with three potential outcomes for Whirlpool’s Free Cash Flow being modeled. Each free cash flow outcome was modeled with an independent percent chance of occurring, which was used to arrive at the expected annual rate of return over the next 10 years at today’s price. For the Upper Band (“UB”), a 3% growth rate was assumed with a 20% chance of occurring. For the Most Likely (“ML”), a 0% growth rate was assumed with a 60% chance of occurring. For the Lower Band (“LB”), a -5% growth rate was assumed with a 20% chance of occurring. At today’s price, that results in an expected annual rate of return over the next 10 years of 6.99%.

WHIRLPOOL CORPORATION’S COMPETITIVE ADVANTAGES AND OPPORTUNITIES

Whirlpool has three competitive advantages that will help them maintain and grow over the next five to ten years:

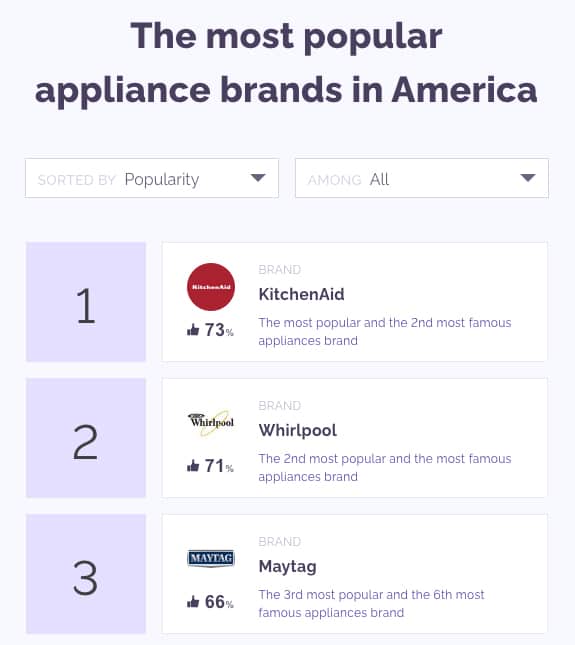

- Branding. Not only does Whirlpool have many brands in its portfolio, but it also has some of the best well-respected brands in the industry. YouGov’s list of “The Most Popular Appliance Brands in America” has three Whirlpool brands at the top of its list

In a competitive industry, which we’ll discuss in the risks section below, branding is very important. As you often see with expensive products, such as automobiles, customers tend to be quite brand loyal. The case is the same for appliances — appliances often are a more expensive item in one’s home. In addition, from my experience in real estate, it seems many individuals prefer to have matching appliance brands across their home, or at least in each room. This means, if a company, such as Whirlpool, is able to sell an individual a refrigerator, they are likely going to try to also buy a Whirlpool dishwasher, stove, microwave, etc. An individual’s brand loyalty deepens a company’s ability to increase its average ticket price and increase sales.

The YouGov article is just one example of many. If you spend time researching the best appliance brands, you will almost always find a Whirlpool brand near the top of the list. It may not always be #1, nor will it always be the flagship “Whirlpool” brand, but a brand in its portfolio is almost always ranked highly when considering “best appliances”.

- Size and scale. According to Statista, Whirlpool was the third largest household appliance company in 2019. Being a large company in a competitive industry, such as the appliance industry, is important for a few reasons. On the customer side, it helps with brand loyalty as people are generally more aware of and familiar with the brand. Financially, larger companies generally have more resources available to them, allowing them to have more leverage and take advantage of more opportunities. Whirlpool is able to buy other brands, and full companies, if necessary, to maintain its competitive edge. While it does not make it impossible for a larger company to be overtaken by a smaller company, as we’ve seen many times before, it does make it a bit more difficult. For example, if Whirlpool were to compete with a smaller startup company that was starting to take market share, it has the resources behind it to compete with the startup if it chose to, or Whirlpool could attempt to use its resources to thwart the threat by buying them out. Whirlpool could also take an approach similar to Amazon and use its leverage to make it very difficult for the startup to continue operating as a standalone business.

- Management. The management team has done a great job of managing the headwinds its industry and business has faced over the previous decade. With a lower quality management team in place over the past decade, Whirlpool likely would’ve gone by the wayside, similar to other narrow-moat businesses in competitive industries. Whirlpool has opportunities ahead, as we will discuss below, but it won’t be without its fair share of challenges. That said, it is going to be facing those challenges with a talented management team at the helm. As long as this management team is in place, it provides a competitive advantage for its business.

Having competitive advantages is important for any business to have sustainable success. In the case of Whirlpool, it is the three main ideas we just discussed previously. However, competitive advantages are not a set-it-and-forget strategy — they are something that must be deepened by continuing to successfully implement new growth opportunities. Without future growth opportunities, a company’s competitive advantage is likely going to be something of the past. For Whirlpool, and investors, there are four opportunities that I see potentially working as it looks to continue to grow:

- Doubling down on what works. A lot of successful business leaders talk and write about how important it is for businesses to double down on what works — put more time, energy, and money into what is actually working. We even talk about this a lot internally here at TIP. This is an opportunity for Whirlpool, that the management team appears to be focusing on. They have a strong business that has been around for a very long-time that is working well. To put it simply, they need to continue doing what they’ve been doing, and continue trying to do it even better. Over the past few quarters, we’ve seen margins expand significantly for Whirlpool. Over the last decade, we’ve seen profitability and free cash flow generation improve significantly, despite stagnating, or declining, sales. This illustrates this idea. Management is focusing on what they’re doing well and trying to do it better by improving its margins. This is an opportunity for the business, and investors, as management finds ways to continue to make the business more efficient and profitable.

- More homeowners. US Census data shows that homeownership rates are actually down over the past two decades, ever so slightly, from about 67.1% in 2000 to 65.8% in the fourth quarter of 2020. Why would I be talking about “more homeowners” being a potential opportunity for Whirlpool? Well, US Census data also shows that homeownership rates jumped from 65.3% in the first quarter of 2020 (pre-COVID) to 67.9% in the second quarter of 2020, which was the first quarter with COVID. The homeownership rate declined through the rest of 2020, but the increase from Q1 to Q2 might indicate truth in reports of people moving from renting in big cities to owning homes in the suburbs. With more people becoming homeowners, this could lead to an influx of new appliance purchases for Whirlpool. This could come in the form of new homeowners remodeling their homes, simply replacing broken appliances from the previous owner, or, as we discussed previously, making all of the appliances across the house match.

- Real estate growth. I wasn’t around in the 80’s, early 90’s, or before that, to see how real estate investing was like back then. Therefore, I cannot compare it to today’s world first hand. However, from numerous conversations with older, successful investors, I’ve learned the real estate investing world has evolved dramatically over the last few decades. This has been driven partially by technology, but also from increased education and access to capital. With more people participating in real estate investing, that leads to more flips and remodels, which leads to more appliance purchases and, indirectly, sales for Whirlpool. As with many previous economic expansions, we’re also seeing more and more new-builds taking place. Each new house, condo, and apartment that gets built needs appliances.

- Dividends. Depending on the price of the stock on any given day, Whirlpool’s dividend yield hovers around 2-3%, currently at 2.35% at the time of this writing. Whirlpool’s management team has demonstrated its focus and priority on maintaining and growing its dividend. It is a profitable and cash generating machine that can afford its dividend payment, which can provide some comfort to investors that worry about a dividend cut. While a focus on high-dividend companies isn’t the right strategy for every investor, for those who do prefer this approach, Whirlpool may be a great option.

RISK FACTORS

Although Whirlpool has competitive advantages and opportunities ahead, it is not without risks that could negatively impact the company and/or prove our financial model to be inaccurate. The major risks for Whirlpool going forward are:

- Competition. The risk of competition is one of my two biggest concerns about the company. This is a risk many market participants are likely aware of — it’s no surprise that there are other major appliance manufacturers in the industry trying to take market share from Whirlpool. There are ways for Whirlpool to defend itself against competition, and even beat its competitors, but there is significant competition and I wouldn’t be surprised if the industry goes through a large disruption in the near future.

- Cyclical and recession. Whirlpool’s business, and the industry as a whole, is very susceptible to cyclical trends. Not only is it cyclical, but it’s also quite tightly correlated to recessions. Appliances are items that most people need in their homes, so if one breaks, they will likely replace it, even in a recession. However, they are likely going to replace it with an affordable option. In recessionary times, people generally don’t splurge on home remodels and appliance upgrades, which negatively impacts Whirlpool’s business.

- Real estate slowing. In the opportunities section above, we just talked about how more homeowners and real estate growth are both opportunities for Whirlpool. Those are both true, there is the possibility of those events occurring, but there is also a risk that neither of those opportunities materialize. If homeowners don’t end up growing or the real estate market slows, that would be a risk to Whirlpool’s business, and could negatively impact investor’s returns.

SUMMARY

Whirlpool Corporation manufactures, markets, and sells major home appliances to markets across the globe. It is a relatively stable company that generates strong cash flows, profits, and is growing, but it does not come without significant risks. It is possible that Whirlpool successfully doubles down on what works, improves margins and profitability, more individuals buy homes and the real estate market continues to boom. However, it is also possible that Whirlpool’s competition significantly erodes its market share, a global recession hits and the real estate market crashes. This is why investing is more often an art than a science.

After reading this investment report, you’re probably wondering – do I buy Whirlpool stock? Well, it’s not quite that simple, and of course, I cannot give specific investing advice, but I will walk you through how I am personally thinking about Whirlpool as an investment.

I was so wrongly approaching value investing when I first got started. I thought I was a value investor by strictly buying companies that looked “cheap” based on my DCF models. I assumed, if my DCF models said the stock was cheap, it was a buy, and I was buying an “undervalued company”. I quickly learned this was not true value investing and that just because I input my assumptions into the DCF model, that didn’t mean they were right or that the market would agree with me.

I also didn’t take into account the momentum of the stock I was considering. Oftentimes, I would buy a company in which I thought was undervalued, then the stock would continue to fall, with negative momentum indicators being clear. I missed the clear negative indicators, causing me to buy into a “falling knife” situation.

As I analyzed Whirlpool, it brought me back to those days in my investing career. On paper, some may argue that Whirlpool seems undervalued and looks like a potentially great investment. If you input certain growth numbers into your DCF models, it can even look significantly undervalued. However, that is purely quantitative and does not take into consideration the future of the business and its qualitative aspects. What I did wrong early in my investing career was exactly that — I did not look at non-financial aspects of the business, nor did I try to think logically about the future of the company and its industry.

Having learned from those experiences and growing as an investor over the past eight years, I am now cautious when considering a business like Whirlpool. Quantitatively, I don’t have many reservations about the company, but qualitatively, I am far more skeptical about the future of its industry, as well as the macro environment as a whole.

In addition, it is not enough to simply analyze a company in a vacuum and make an investment decision. Investors must compare their expected return of one investment to that of another option available. Your dollar can only be invested in one place at a time — choosing the optimal place for that dollar to be invested is equally as important, if not more important.

According to our TIP Finance Momentum tool, Whirlpool is currently green, meaning it has positive momentum. This helps alleviate my concern for a potential falling knife situation. However, from a qualitative perspective, I am not convinced that Whirlpool will be able to continue to thrive in this industry, nor am I convinced that Whirlpool is the best place to invest my dollar at this point in the cycle.

Nearly all companies have a price in which it is a good buying opportunity. With Whirlpool being a cyclical business, it is possible that the valuation of the company will swing drastically in the other direction and be, in my opinion, significantly undervalued. In that event, I would consider starting a small position in a company like Whirlpool. However, at today’s price, I personally am not purchasing Whirlpool stock.

To learn more about intrinsic value, check out our comprehensive guide to calculating the intrinsic value of stocks.

Disclosure: The author, Robert Leonard, as of this writing, of the companies mentioned, only holds a long position in Square, Inc. (SQ), with no intentions of initiating a position in any other company mentioned in this article within the next 72 hours. The article was written himself, and it expresses his own opinions. He is not receiving compensation for it (other than from The Investor’s Podcast Network). He has no business relationships with any company whose stock is mentioned in this article. The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Robert is not a financial advisor. Please always do further research and do your own due diligence before making any investments.