Skip to content

Skip to content Intrinsic Value Assessment Of Expedia Inc. (EXPE)

By Stephen Barnes From The Investor’s Podcast Network | 13 January 2019

INTRODUCTION

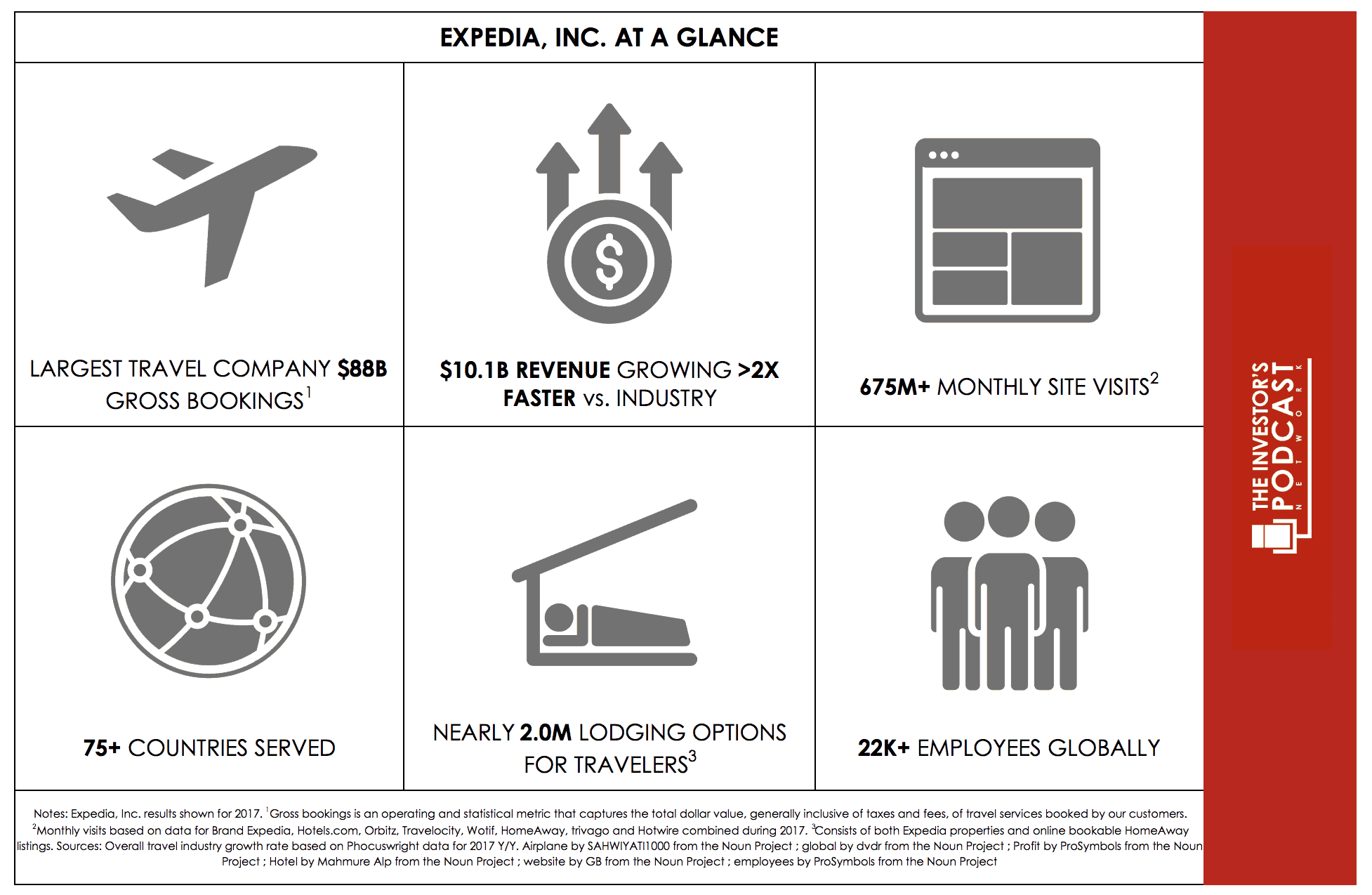

Expedia, Inc. is an online travel company that provides leisure travelers and businesses with the technology, tools, and information they need to plan, book, and experience travel. Expedia owns and controls a broad portfolio of travel brands and is the world’s largest travel agency by bookings.

Expedia derives the majority of its revenues from lodging and accommodations services (68% of sales in 2017). The remainder of its revenues is derived from services for air tickets (8%), rental cars, cruises, in-destination, and others (13%), and advertising (11%).

Source: Expedia Inc., Investor Presentation of February 8, 2018

Source: Expedia Inc., Investor Presentation of February 8, 2018

Travel suppliers distribute and market products via Expedia’s desktop and mobile offerings (apps), as well as through alternative distribution channels, and Expedia’s private label business. Expedia also operates an advertising and media business that helps other businesses, mainly travel providers, reach a large audience of travelers around the globe.

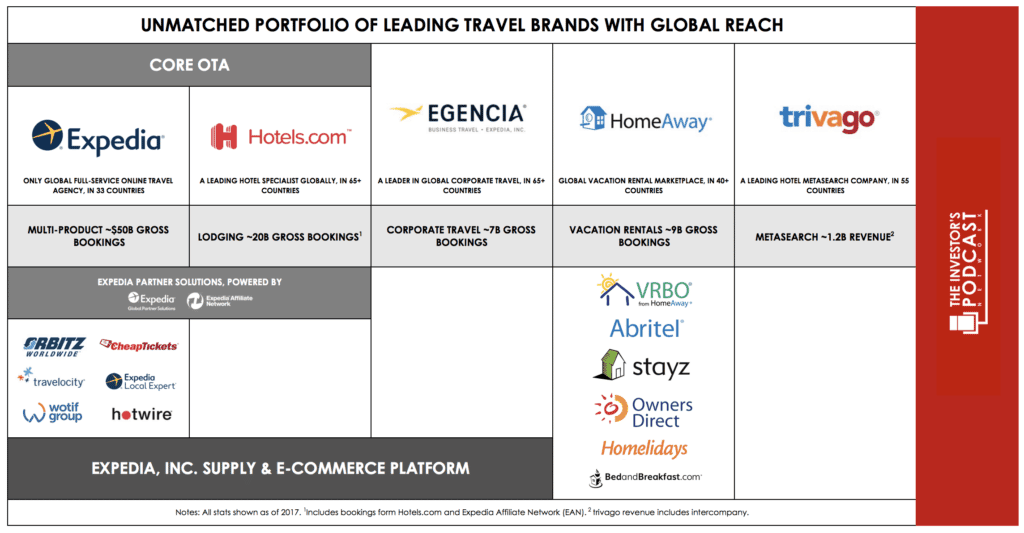

Expedia’s portfolio of brands and businesses include the following, among others:

- Expedia.com®, a leading full-service online travel company with localized websites in 33 countries;

- Hotels.com®, a leading global lodging expert operating 90 localized websites in 41 languages with an award-winning loyalty program (book ten nights, get one free);

- Expedia® Affiliate Network, a global B2B brand that powers the hotel business of hundreds of leading airlines, travel agencies, loyalty, and corporate travel companies plus several top consumer brands through its API and template solutions;

- trivago®, a leading online hotel metasearch platform with websites in 55 countries worldwide;

- HomeAway®, a global online marketplace for the vacation rental industry with nearly 1.8 million online bookable vacation rental listings, which also includes the VRBO, com, and BedandBreakfast.com brands, among others. These brands compete with the popular and fast-growing Airbnb. In addition to its online marketplace, HomeAway also offers software solutions to property managers through its HomeAway Software and Glad to Have You products. On October 25, 2018, Expedia also announced the acquisition of Pillow and ApartmentJet, which will be folded into HomeAway portfolio of companies;

- Egencia®, a leading corporate travel management company;

- Orbitz® and CheapTickets®, leading U.S. travel websites, as well as ebookers®, a full-service travel brand with websites in seven European countries;

- Travelocity®, a leading online travel brand in the United States and Canada;

- Hotwire®, a leading online travel website offering spontaneous travel deals;

- Expedia® Media Solutions, the advertising sales division of Expedia, Inc. that builds creative media partnerships and enables brand advertisers to target a highly-qualified audience of travel consumers;

Source: Expedia Inc., Investor Presentation of February 8, 2018

The Company’s current market cap is about $17.01 Billion, and its enterprise value (i.e., market cap + total debt net of cash) is approximately $18.77 Billion. During the most recent twelve-month period, it generated $15.7 Billion in sales and $1.2 Billion in levered free cash flow (i.e., after interest expense), or $1.5 billion in unlevered free cash flow (i.e., before interest expense). The company’s common stock has fluctuated between a high of $139.77 and a low of $98.52 over the past 52 weeks and currently stands at around $114.56. Is Expedia undervalued at the current price?

THE INTRINSIC VALUE OF EXPEDIA, INC.

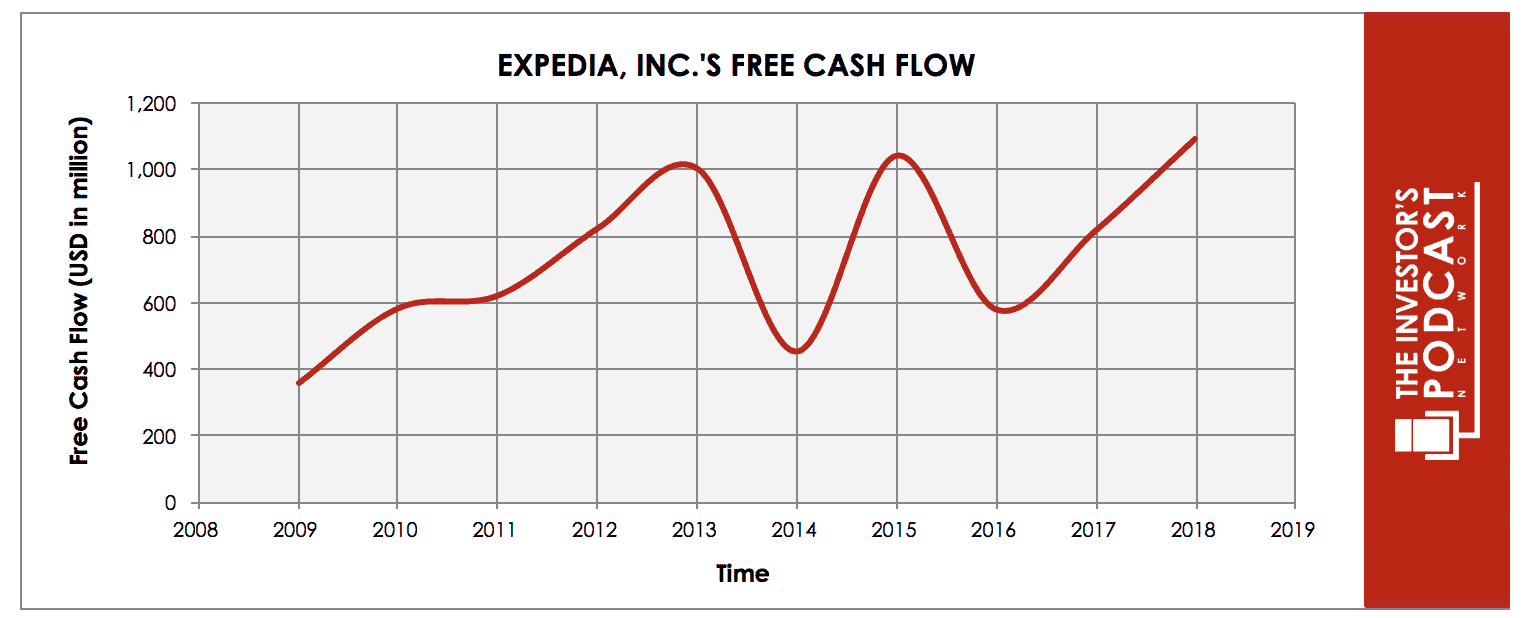

To determine the intrinsic value of Expedia, we’ll start by looking at the company’s historical free cash flow. A company’s free cash flow is the true earnings which management can either reinvest for growth or distribute back to shareholders in the form of dividends and share buybacks. Below is a chart of Expedia’s free cash flow for the past ten years.

As one can see from the chart above, the company’s free cash flow has grown over the last ten years, from $361 million in 2008 to $1.2 billion in the twelve-month period through September 2018. In other words, free cash flow grew at a compound annual growth rate (CAGR) of 12.76% over the past ten years.

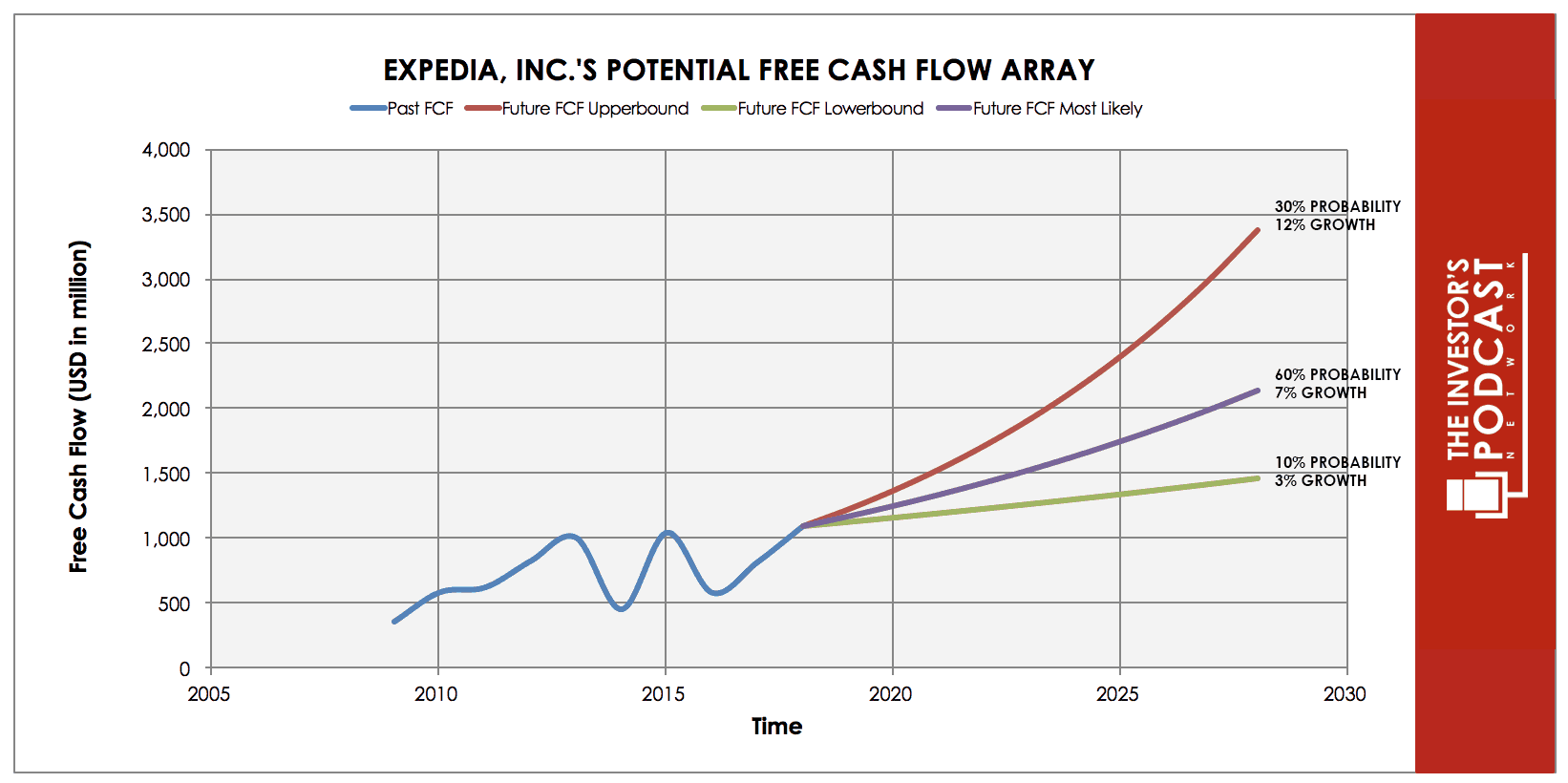

To determine Expedia’ intrinsic value, an estimate must be made of its potential future free cash flows. To help us build this estimate, we have calculated and displayed an array of potential outcomes for future free cash flows below.

When examining the array of lines moving into the future, each one represents a certain probability of occurrence. The upper-bound line represents a 12% growth rate which is slightly less than the 12.76% compounded annual growth rate (CAGR) achieved over the past ten years. This 12% growth rate has been assigned a 30% probability of occurrence as it is certainly possible, but perhaps not the most plausible scenario since companies typically grow slower and slower as they mature and as revenues get larger. However, in Expedia’s case, three factors argue in favor of a 12% growth rate.

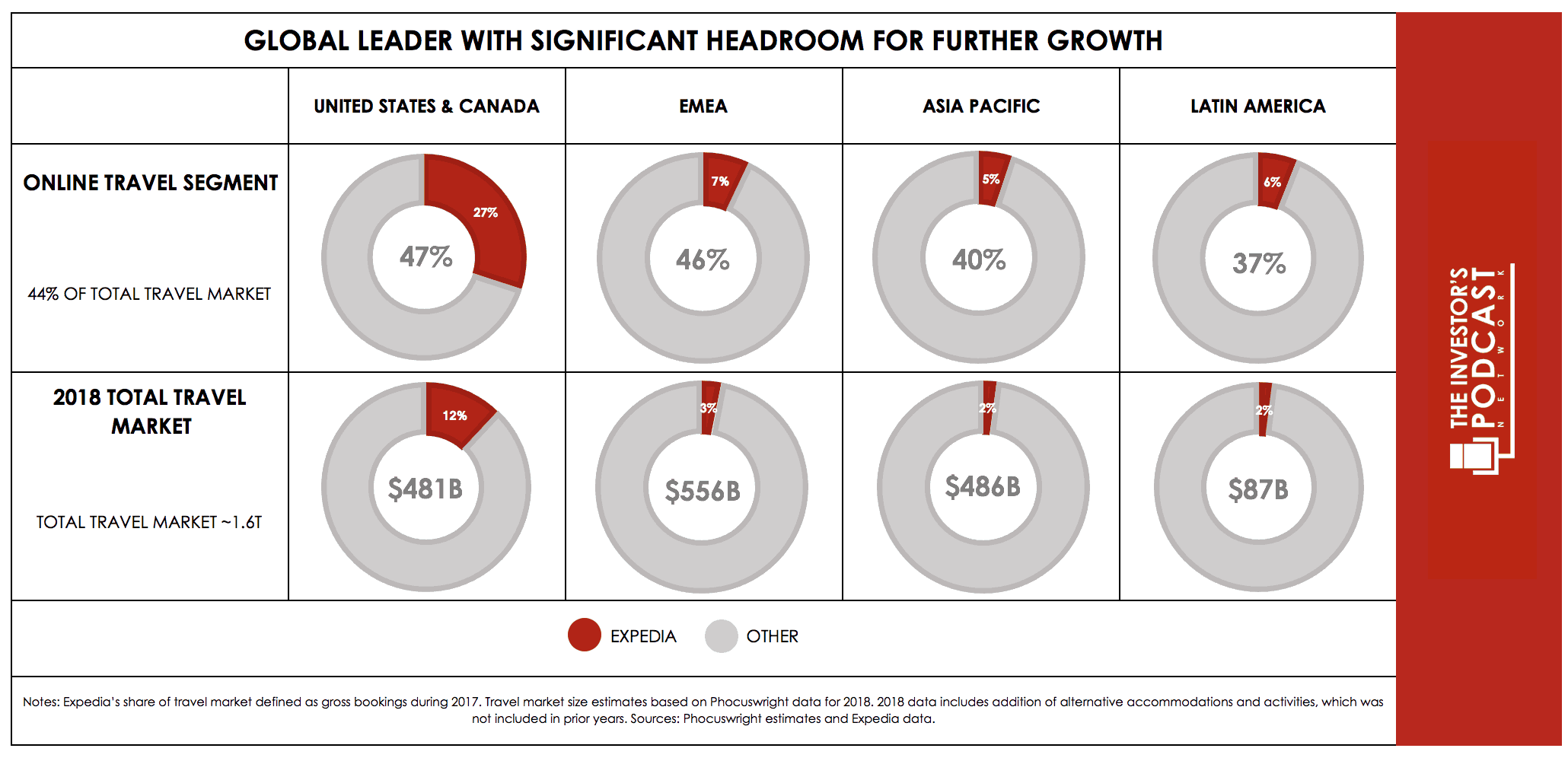

First, the market in which it competes is huge. The global travel market was estimated to be about $1.6 trillion in 2018, and the online travel segment of that market is still less than half (44% of the global travel market) and even a smaller percentage outside the U.S. (7% in EMEA, 6% in LATAM, and 5% in APAC).

Source: Expedia Inc., Investor Presentation of February 8, 2018

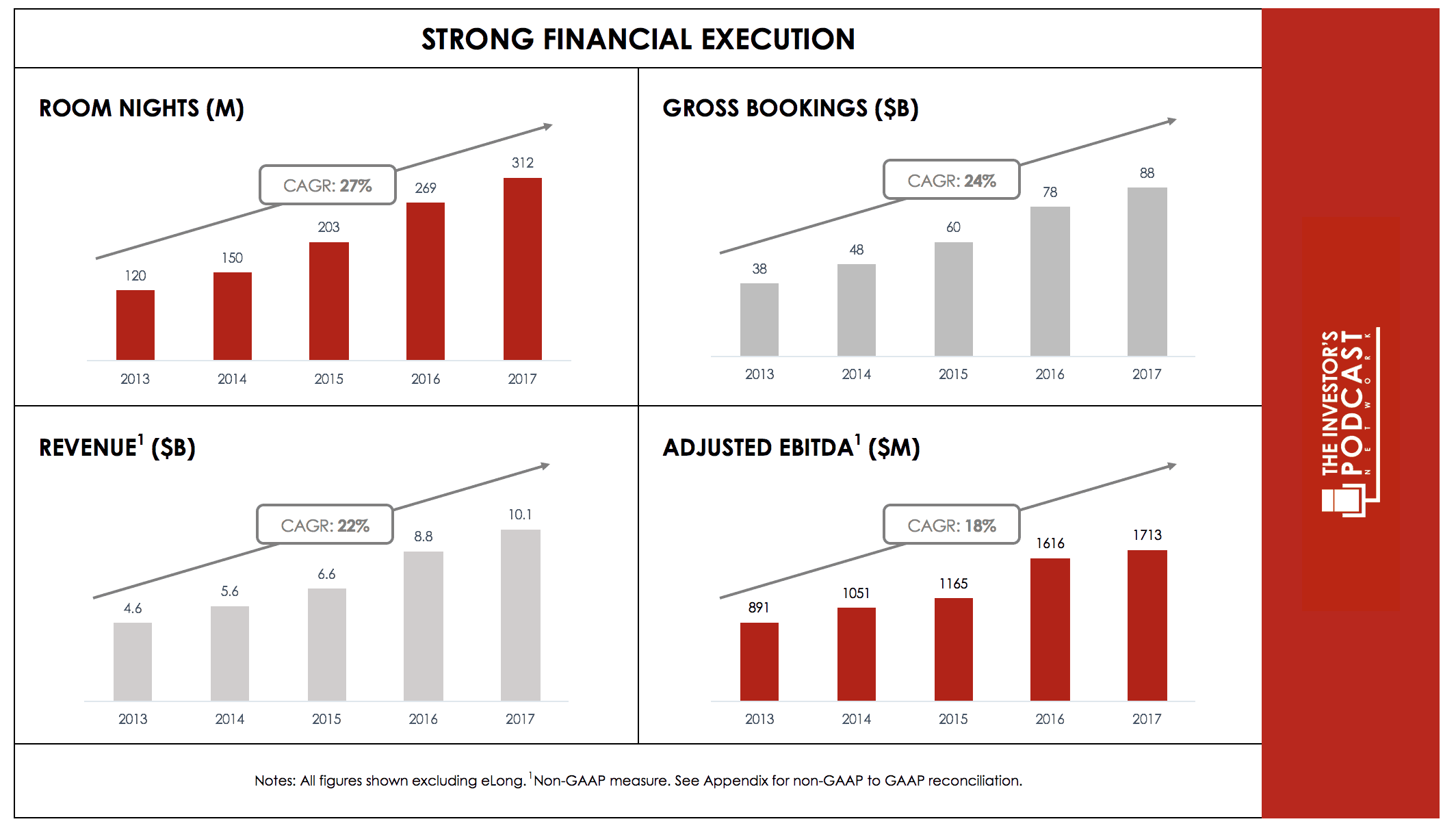

Second, during the five-year period from 2013 through 2017, revenue grew at a CAGR of 22% while Adjusted EBITDA (somewhat of a proxy for cash flow) grew at a CAGR of 18%.

Source: Expedia Inc., Investor Presentation of February 8, 2018

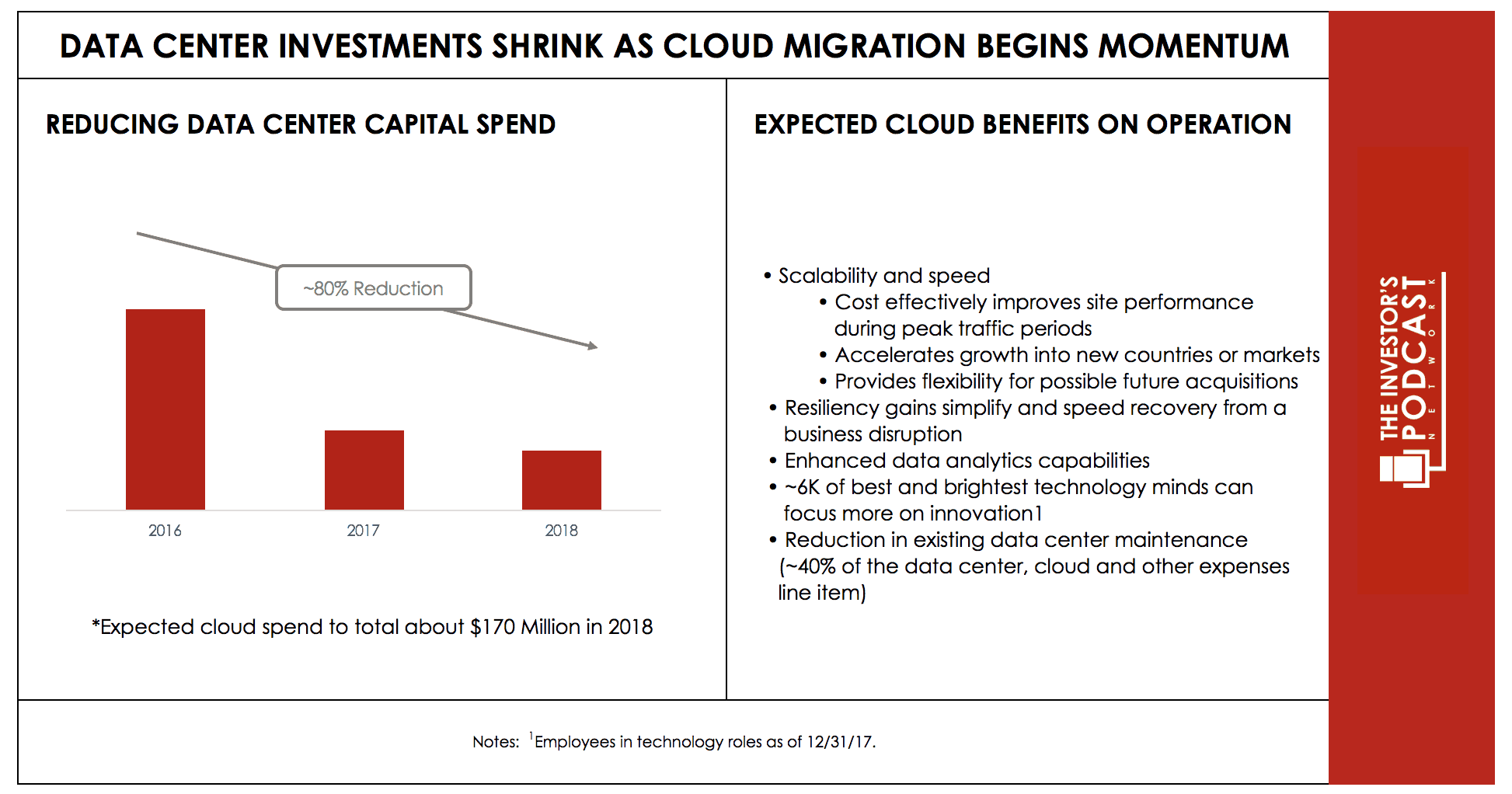

Third, certain capital expenditures, such as data center investments, are shrinking as Expedia migrates to the cloud.

Source: Expedia Inc., Investor Presentation of February 8, 2018

To account for a number of factors including fierce competition and promotional activity among branded food manufacturers and private-label products as retailers consolidate, offset somewhat by potential revenue and earnings increases from future acquisitions.

The middle growth line represents a 7% growth rate to account for a number of factors including fierce competition in the online travel space and the plausibility of slowing global economic growth and/or a recession in the near term. Expedia’s competitors include well-capitalized online and offline travel companies, large online portals and search websites, certain travel metasearch websites, mobile travel applications, social media websites, as well as traditional consumer e-Commerce and group buying websites. The middle growth scenario has been assigned a 60% probability of occurrence, as it is most likely to occur.

The lower bound line represents a 3% growth rate in free cash flow and assumes that the company will grow at about the same rate as the 10-Year Treasury Note, which is a good proxy for projected GDP growth (i.e., the growth of the overall economy) over the next ten years. Expedia is very likely to grow at least as fast as the overall economy. This scenario has been assigned only a 10% probability, as the company will most likely grow much faster than the overall economy given the vast market in which it competes and the global trend from offline to online bookings.

Assuming these potential outcomes and corresponding cash flows are accurately represented, Expedia might be priced to generate a 9.4% annual return if the company can be purchased at today’s price of $117. Let’s now take a look at another valuation metric to see if it corresponds with this estimate.

Based on Expedia’s current earnings yield, which is the inverse of its EV/EBIT ratio, the company is currently yielding 4.5%. This is below the Consumer Discretionary Sector median average of 7.6% suggesting that the company may be overvalued on a comparable basis. However, Expedia has a current EV/LTM Free Cash Flow yield of 7.1%. This is above the Consumer Discretionary Sector median average of 5.3% suggesting that the company may be undervalued on a comparable basis. Finally, we’ll look at Expedia’s free cash flow yield, a

metric which assumes zero growth and simply measures the firm’s trailing free cash against its current market price or market capitalization. At the current market price, Expedia has a free cash flow yield of 6.9% compared to 5% for the Consumer Discretionary Sector.

Taking all these points into consideration, it seems reasonable to assume that Expedia is currently trading at a discount to fair value. Furthermore, the company may return around 9.4% annually at the current price if the estimated free cash flows are achieved. Now, let’s discuss how and why these estimated free cash flows could be achieved.

THE COMPETITIVE ADVANTAGE OF EXPEDIA, INC.

Expedia has various competitive advantages outlined below.

- Brand Value. One of Expedia’s most powerful competitive advantages is its portfolio of recognizable brands. Expedia sells its travel offerings under numerous leading and trusted brands (see the list of brands in the introduction section above). Expedia can leverage these brands to garner trust with customers when making large travel purchases.

Source: Expedia Inc., Investor Presentation of February 8, 2018

For a competitor to challenge Expedia’s competitive brand position, they would have to deploy a large amount of capital and resources on advertising, customer service, and distribution. In fact, in 2017, Expedia spent $4.36 billion on direct selling and marketing activities.

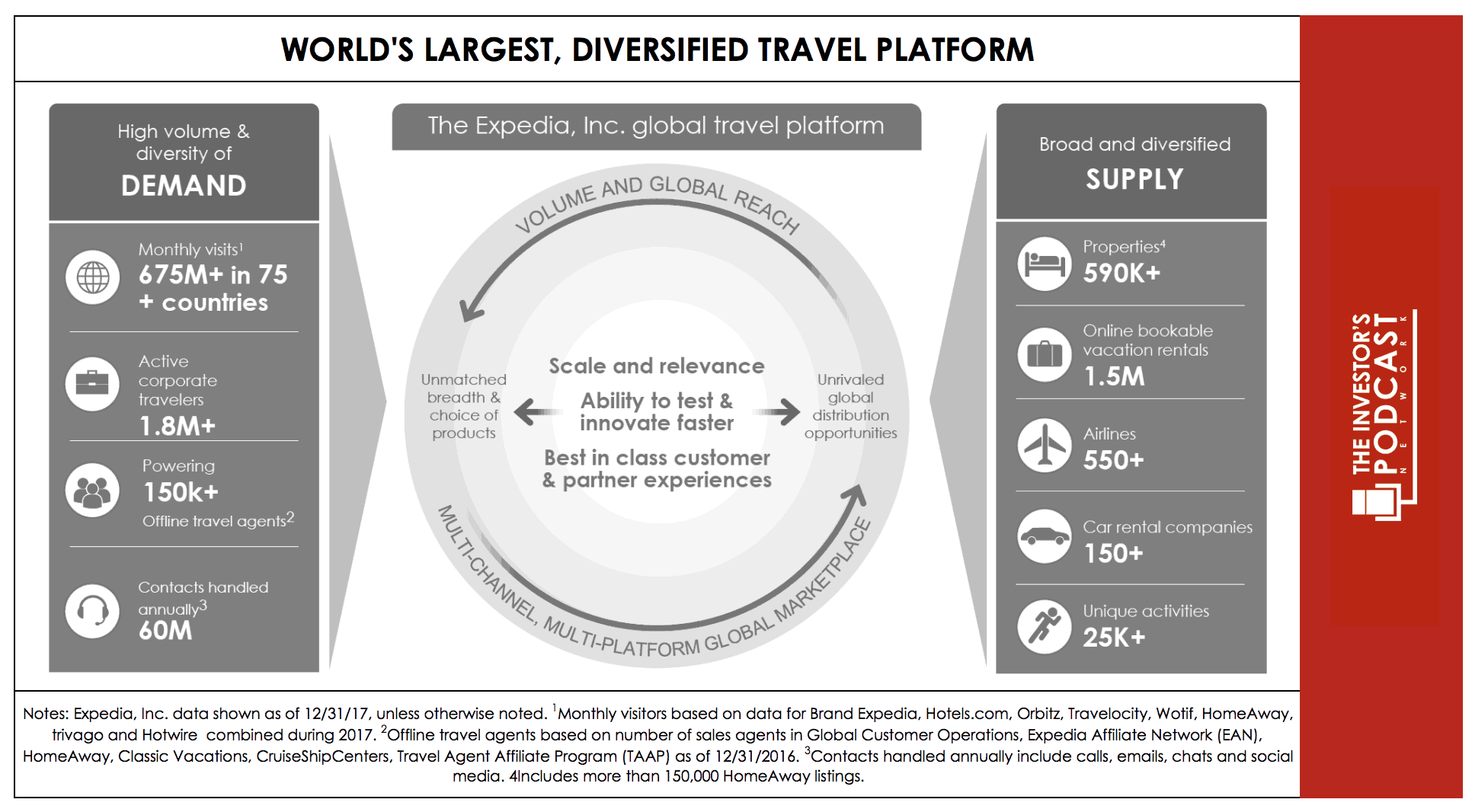

- Strong Network Effects. Expedia has built and continues to build, a broad network of travel offerings. On the supply side, as of September 30, 2018, the core Expedia platform exhibited 895,000 properties, and HomeAway sported nearly 1.8 million bookable listings. On the demand side, as measured by App Annie on October 25, 2018, Expedia’s core platform ranks as a top-10 journey iOS mobile application in 17 countries versus 118 for Booking.com, and 25 for TripAdvisor.

Source: Expedia Inc., Investor Presentation of February 8, 2018

This strong network effect has led Expedia to become one of two dominant players in the global online travel agency booking market—the other player being Booking Holdings (formerly known as Priceline). Expedia and Booking each have about 35% share in the global online travel agency booking market. The number three player, Orbitz, was acquired by Expedia in 2014.

Beneath Expedia and Booking, market share is highly fragmented, making it very hard for smaller players to gain customer traffic and supplier scale. Smaller players would need to expend large amounts of capital and substantial human capital to build relationships with hotels and gather critical accommodation information, including pictures, just to get started. Then, to attract customers, they would need to spend heavily on advertising to attract customers to their app or website (as mentioned, Expedia spent over $4.3 billion or 43% of revenue on direct marketing in 2017). And even if a smaller player managed to attract a few customers, it would need to build out IT systems, data centers, and a 24/7 customer support team to retain them. Not an easy task!

- Switching Costs. Finally, Expedia’s scale allows it to economically offer rewards and loyalty programs to its customers. Once Expedia wins a customer, its rewards and loyalty programs incentivize the customer to book with Expedia or one of its brands again and make it hard to switch to a competitor. For instance, Hotels.com Rewards®, the loyalty program established in 2008, offers travelers the ability to earn one free night for every ten nights stayed. I personally have taken advantage of this rewards program and was reluctant to book a hotel through any site other than Hotels.com. Beyond Hotel.com Rewards®, Expedia offers Expedia®+ rewards on over 30 Brand Expedia points of sale, as well as Orbitz Rewards on Orbitz.com.

EXPEDIA, INC.’S RISKS

Now that Expedia’s competitive advantages have been considered let’s look at some of the risk factors that could impair our assumptions of investment return.

- Potential competition for well-capitalized mega companies. Expedia may encounter meaningful competition over the next ten years from mega companies that already have the pocketbooks and user traffic necessary to build network scale and the desire to enter a $1.6 trillion market for the sake of growth. These potential new entrants include Google, Facebook, Amazon, Alibaba, Baidu,TripAdvisor, and hotel consortia. Focused entry by any one of these competitors could lead to industry commodification and margin contraction. That said, the market can probably support some level of increased competition over the next several years, as the travel booking market is extremely large, at $1.6 trillion, and online penetration of the travel market remains low, especially outside the United States.

- Growth in Alternative Accommodations Market. The explosive growth experienced over the past few years in the alternative accommodations market (think Airbnb) has taken many travel companies by surprise. Continued growth and transition toward alternative accommodations could hamper Expedia’s core platform business. However, this may be offset by Expedia’s HomeAway segment, which competes in the alternative accommodations space and directly against Airbnb. In fact, Expedia’s HomeAway segment has experienced 35% year-over-year revenue growth and 66% year-over-year Adjusted EBITDA growth over the last two years. In the most recent quarter (ending September 2018), HomeAway accounted for approximately 12% of total revenue, up from 10.3% a year ago.

- Lower Bookings in Economic Downturn. Finally, an economic downturn could negatively impact Expedia’s results. The travel industry is cyclical and affected by changes in economic growth. During economic downturns, consumers have typically cut leisure travel before many other expenses. During the 2009 downturn, when Expedia was still a young and growing company, sales were flat. If a downturn were to occur today, now that Expedia is mature, it would probably experience a decline in sales.

OPPORTUNITY COSTS

Whenever an investment is considered, one must compare it to any alternatives to weigh up the opportunity cost. At the time of writing, 10-year treasuries are yielding 2.731%. If we take inflation into account, the real return is likely to be closer to 1%. The S&P 500 Index is currently trading at a Shiller P/E of 28.5 which is 69.64% higher than the historical mean of 16.8. Assuming reversion to the mean occurs, the implied future annual return is likely to be -2.8%. Expedia, therefore, appears to offer a much better return for investors at present, but other individual stocks may be found which offer a similar return relative to the risk profile.

MACRO FACTORS

Investors must consider macroeconomic factors that may impact economic and market performance as this could influence investment returns. At the time of writing, the S&P is priced at a Shiller P/E of 28.5. This is 69.64% higher than the historical average of 16.8 suggesting markets are at elevated levels. U.S. unemployment figures are at a 30-year low suggesting that the current business cycle is nearing its peak. U.S. private debt/GDP currently stands at 199.6% and is at its highest point since 2009 when the last financial crisis prompted private sector deleveraging.

SUMMARY

Expedia is competitively positioned given advantages that are difficult for competitors to replicate: (1) a stellar portfolio of well-known and trusted travel brands, (2) network effects created by apply supply and demand, and (3) switching cost advantages created by its ability to offer rewards and loyalty programs at scale.

Expedia is well-positioned in a large and growing global travel market. As mentioned above, it is one of two dominant players and odds are that it won’t be displaced from the duopoly anytime soon. Furthermore, it is worth noting that the future looks bright for the company’s HomeAway segment, which continues to grow alongside Airbnb in the popular alternative accommodations market. In fact, earlier this year, Airbnb was valued at 31 billion dollars in the private market, which is much higher than Expedia’s current enterprise value of about $18-19 billion.

In short, Expedia’s shares look attractively valued. Indeed, based on the assumptions used in the analysis above, Expedia may return around 9.7% to shareholders annually if purchased at the current market price of $114.20. Assuming that diversified market investors generally require a 7% annual rate return (equating roughly to a 14x earnings multiple), then it stands to reason that Expedia is trading at about a 38-39% discount ([9.7% – 7%]/7% = 0.3857) at current prices.

To learn more about intrinsic value, check out our comprehensive guide to calculating the intrinsic value of stocks.

Disclaimer: The author does not hold ownership in any of the companies mentioned at the time of writing this article.